Statement of Functional Expenses: A Nonprofit Guide

A statement of functional expenses shows where your nonprofit's money went, and why. It breaks every expense into two dimensions: what you bought (salaries, rent, supplies) and what purpose it served (programs, administration, fundraising).

For nonprofits with gross receipts over $200,000, it’s not optional. It’s required for GAAP compliance and Form 990 filing. But beyond compliance, it’s the document your auditors, board, and major donors will use to judge whether you’re spending responsibly.

This guide walks you through what it is, how to prepare it, and the allocation mistakes that trip up even experienced finance teams.

What Is a Statement of Functional Expenses?

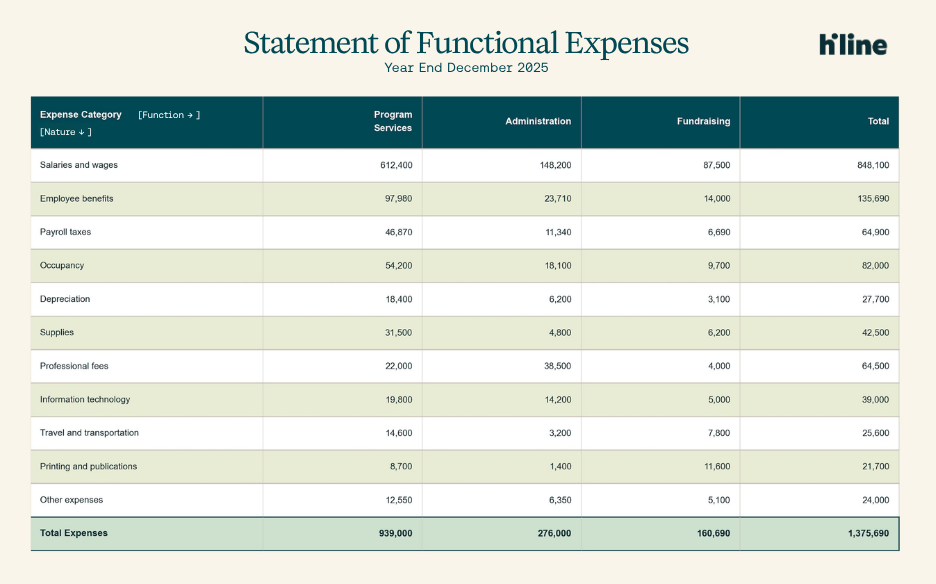

The statement of functional expenses is a matrix.

Every line item appears twice: once classified by nature (what was purchased — salaries, rent, supplies, professional fees) and once classified by function (what purpose it served — program delivery, administration, or fundraising). The resulting grid shows exactly how much you spent on each natural expense category across each functional area.

There isn’t a for-profit equivalent for this. This statement is unique to nonprofits and is one of four core nonprofit financial statements, alongside the Statement of Financial Position, Statement of Activities, and Statement of Cash Flows.

The definition is the easy part. The allocation is the complex part, which is what we’ll cover in the rest of this guide.

Who Is Required to Prepare One?

FASB ASC 958 Requirements

Under FASB ASC 958, all nonprofits must show their expenses by both function and nature.

There are three acceptable formats:

- A standalone statement

- A schedule in the notes to financial statements

- Integrated within the Statement of Activities

Most organizations use the standalone format because auditors and boards find it easier to read.

Form 990 Filers

The IRS requires nonprofits to complete Part IX of the Form 990, which is essentially the statement of functional expenses, if the organization has:

- Gross receipts of $200,000 or more, or

- Total assets of $500,000 or more

Even organizations that fall below those thresholds will encounter the statement in audits and major grant applications. So whether it’s technically required, we always recommend to include it.

The Three Functional Expense Categories

Let’s break down each of the expense categories that your statement should include in more detail.

1. Program Services

Program costs are directly tied to delivering the mission: salaries of staff who run programs, supplies consumed by programs, direct program costs.

It’s also the most scrutinized category. Donors and watchdog organizations use the program expense ratio (program expenses as a percentage of total expenses) as a quick proxy for organizational health.

Staff who split their time across programs and administration can allocate a portion of their salaries to program services. But the kicker is that you have to document the split, or the allocation doesn’t hold up in an audit.

For example, a program manager who spends 20% of their time on administrative tasks should have 80% of their salary classified as program services, with documentation to support it. Under-documenting this understates your program expenses and misrepresents your actual spending to donors.

2. Administration

Administration, often known as Management and General (M&G), covers overhead: governance, accounting, HR, executive leadership not tied to a specific program. Most organizations want to minimize this category for donor optics, which could get you in hot water down the line.

Shifting costs out of M&G without a defensible basis doesn’t reflect what’s actually happening in the organization, and auditors will find it.

3. Fundraising

Fundraising covers all costs related to soliciting donations, running campaigns, and cultivating major donors, including staff time spent on donor relations, direct mail costs, event fundraising expenses, and online campaign costs.

Over-allocating expenses to fundraising is a red flag. Charity Navigator and GuideStar even penalize organizations with high fundraising expense ratios, and sophisticated major donors know the benchmarks.

Worth noting separately: membership development is a distinct subcategory that many organizations miss entirely. It belongs in fundraising, not program services, unless the membership activity is itself mission work.

How to Prepare a Statement of Functional Expenses

Step 1 — List All Natural Expense Categories

Start with a complete list of natural expense categories: salaries and wages, employee benefits, payroll taxes, occupancy, depreciation, supplies, travel, printing, professional fees, information technology, and any other material to your organization.

GAAP doesn’t prescribe a specific number of categories, but generally, about five to ten is the norm. Keep the natural categories consistent year over year. If you change categories all the time without a documented reason, this makes trend analysis impossible and creates auditor questions.

Step 2 — Identify Direct Expenses

Direct expenses belong clearly to a single functional category. For example

- A program manager whose job description covers only program work: 100% Program Services

- A development associate whose role is entirely fundraising: 100% Fundraising

Tag these directly in your accounting system throughout the year. Leaving direct expenses in a general account to sort out at year-end is where miscoding happens.

For single-function employees, the job description is sufficient documentation. No timesheets required.

Step 3 — Allocate Shared (Indirect) Expenses

This is where the statement gets difficult, and where most organizations become inconsistent.

You have to allocate shared costs, primarily personnel costs for employees who serve multiple functions, across functional categories using a documented, reasonable basis.

Personnel costs are the biggest shared expense category and the most scrutinized. Make sure you get it right by using one of these three accepted methods:

- Time and effort (timesheets) – The most defensible. Staff log actual hours by function. Allocation follows the time record. Auditors have no grounds to challenge a timesheet-based allocation applied consistently.

- Job description basis – For employees who clearly serve one primary function with limited spillover. Simpler than timesheets, defensible if the job description is current and the allocation is documented.

- Time studies – Periodic snapshots of how employees actually spend their time, conducted at representative intervals. Acceptable as a reasonable estimate when timesheets aren’t practical. Must be documented and updated when roles change significantly.

For non-personnel shared costs, common allocation bases include:

- Occupancy – Allocate by square footage used by each functional area

- Technology costs – Allocate by headcount or system usage by function

- Depreciation – Allocate based on how the asset is used across functions

Finally, you have to apply the allocation method consistently year-over-year. Switching from headcount to square footage between years, without a documented reason, is an audit finding waiting to happen.

Step 4 — Build the Matrix

Once direct expenses are tagged and shared costs are allocated, the statement takes shape:

- Rows = natural expense categories (salaries, rent, supplies, etc.)

- Columns = functional categories (Program A, Program B, Management & General, Fundraising)

- Final column = Total expenses

The totals must reconcile with your Statement of Activities. If they don’t, find the discrepancy before the auditors do.

Step 5 — Document Your Methodology

A written cost allocation plan documents which allocation basis you used for each shared cost category, how it’s calculated, and who is responsible for updating it. Auditors will ask for this document.

“We use reasonable allocations” is not a documented methodology. The absence of a written plan is itself an audit finding, even if every number on the statement is accurate.

Update the plan annually if your organizational structure, programs, or staff roles have changed materially. A plan written three years ago that doesn’t reflect how the organization currently operates creates more exposure than no plan at all.

When your books are managed by an expert team, the allocation methodology is built into your chart of accounts from day one, not reconstructed at year-end. See how Hiline works with nonprofits →

Common Mistakes That Create Audit Exposure

- Misclassifying admin as program – Inflates the program expense ratio and holds up fine until auditors review the underlying job descriptions or timesheets.

- Allocating M&G expenses to programs without basis – Overhead costs belong in M&G. Moving them without documentation is a reporting error.

- Inconsistent allocation methods year-over-year – The methodology itself is the audit trigger, not just the numbers.

- Ignoring indirect costs entirely – Understates the true cost of delivering programs and distorts the financial picture for board decision-making.

- Over-allocating to fundraising – Watchdogs and major donors know the benchmarks. The statement should reflect what actually happened.

- No written cost allocation plan – The most common finding. A correct allocation without documentation still gets flagged.

What Does a Healthy Program Expense Ratio Look Like?

Most watchdog organizations consider 65 to 75% in program expenses the baseline for a financially responsible nonprofit. That’s 65 to 75 cents of every dollar going toward mission delivery, with the remainder covering administration and fundraising.

Charity Navigator awards top marks (four stars) to organizations that spend 85% or more on programs.

A nonprofit in its first two years will naturally carry higher administrative and fundraising costs as it builds infrastructure. An organization mid-capital campaign will see fundraising expenses spike. Neither is a problem if the board can articulate why.

What about when the ratio is lower than ideal or you’re just starting out? Examine the actual spending mix, ask whether the overhead costs are sustainable, and build a plan to grow program delivery as the organization scales.

Overall, auditors and sophisticated funders just want a ratio that’s consistent year over year, with movement explained by documented organizational decisions.

Statement of Functional Expenses vs. Form 990 Part IX

Most nonprofits effectively prepare this statement twice: once for the audit (as a standalone statement) and once for the 990 (Part IX).

Not a problem… if the two reconcile. If the numbers in Part IX don’t match the audited statement, that discrepancy surfaces in the audit review, in board oversight, and potentially with the IRS.

The most common reason for a mismatch: the 990 preparer, often an external CPA, applies different expense classifications than the internal accounting team used during the year. Fix this by giving the 990 preparer the audited statement of functional expenses and confirming that Part IX is built from the same underlying data.

Frequently Asked Questions

Is a statement of functional expenses required for all nonprofits?

FASB requires all nonprofits to report expenses by function and nature. Nonprofits with gross receipts over $200,000 or total assets over $500,000 must also include it in their Form 990 filing. Even organizations below those thresholds will encounter it in audits and major grant applications.

What are the three functional expense categories?

Program services (mission-delivery costs), management and general (overhead and administration), and fundraising (donor solicitation and campaign costs).

What’s the difference between functional and natural expense classification?

Functional classification describes why money was spent, which program or activity it served. Natural classification describes what was purchased, salaries, rent, supplies. The statement of functional expenses reports both in a matrix format.

How do nonprofits allocate shared expenses?

Shared costs are allocated using a documented, consistent method, typically based on time spent (timesheets), square footage, or headcount. Personnel costs are most commonly allocated by time and effort.

What is a good program expense ratio for a nonprofit?

Most watchdog organizations consider 65 to 75% in program expenses healthy. Charity Navigator awards top marks to organizations that spend 85% or more on programs. The right ratio depends on organizational size, age, and current strategic priorities.

Ready to stop rebuilding your allocation methodology every year? Hiline builds it into your books from day one, so your statement of functional expenses is always audit-ready. Book a free consultation with Hiline →

Sign up for our newsletter.

.png)