Your statement of activities (SOA) is the financial document that answers the question every donor, board member, and grant officer is actually asking: Did you use our money well?

It’s the nonprofit equivalent of an income statement, tracking every dollar that came in and every dollar that went out during a specific period.

This article breaks down what goes into a statement of activities, how to read one, and what your numbers are actually telling you. We’ve even thrown in a template you can use or adapt to your organization.

What Is a Statement of Activities?

A statement of activities tracks all of a nonprofit’s revenue earned and expenses incurred during a reporting period (typically a fiscal year) and shows the change YoY in net assets.

Under GAAP, it is one of four required financial statements, alongside the statement of financial position, the statement of cash flows, and the statement of functional expenses. It also feeds directly into your Form 990. Most importantly, auditors, grantors, and state regulators will reconcile what they see here with what you report to the IRS.

The 3 Core Components of a Statement of Activities

Revenue

Revenue includes all incoming funds: individual donations, foundation grants, government funding, program service fees, special events, and in-kind contributions. In-kind contributions (donated goods and services) must be recorded at fair market value. Leaving them out understates both revenue and expenses.

Expenses

Expenses are broken into three functional categories:

- Program services — The direct cost of delivering your mission

- Management and general — Overhead: governance, accounting, HR, executive leadership

- Fundraising — Campaigns, events, donor cultivation

Auditors, grantors, and watchdog organizations use this breakdown to calculate your program expense ratio — how much of every dollar actually went toward mission delivery.

Change in Net Assets

Also known as the bottom line, or the difference between total revenue and total expenses. If you ended with a surplus, this may include restricted funds that aren’t freely available (more on this below). Or a planned deficit draw against reserves could be dictated by your board. What matters most here is the story behind the number.

Restricted vs. Unrestricted Funds: Why This Matters on Your Statement of Activities

Not all money that comes in is yours to spend freely. That's the whole concept.

Some donors write a check and say "use this however the organization needs." Others write a check and say "this is for the after-school program only" or "spend this by December 31." Same dollar amount. Completely different situation.

The first type is "unrestricted". The second is "restricted". Your statement of activities shows both in separate columns, so anyone reading it can see exactly how much of your revenue is truly flexible and how much is earmarked. Think of it like this:

- Without donor restrictions – Money the organization can use for any mission-related purpose

- With donor restrictions – Money a donor or funder has designated for a specific program, time period, or purpose

Why the split matters more than the total

A nonprofit can show $200,000 in net assets and still be in serious trouble. If $190,000 of that is tied to a specific grant, the organization only has $10,000 it can actually use for day-to-day needs. Grant officers and auditors know to look at the columns — not just the total at the bottom.

Releases from restriction

When you spend restricted money on what the funder intended, one more step is required: recording a *release from restriction*. Think of it as officially moving that money from the "earmarked" pile to the "spent as directed" pile in your books.

Skip it, and your restricted balance looks higher than it actually is. That's a bookkeeping error auditors will find.

Nonprofit Statement of Activities Template (+ How to Use It)

Every organization’s SOA will look slightly different based on your chart of accounts and program structure. Most accounting software generates this report automatically if your chart of accounts is set up correctly but you can also use this template to get started on your own.

If your SOA looks messy, or if the restricted/unrestricted split seems off, that’s usually a signal the underlying bookkeeping needs attention, not just the report.

Hiline can help with that if you’re stuck. Just reach out to our nonprofit team for a free consultation.

How to Read Your Statement of Activities (What the Numbers Are Telling You)

Preparing the statement is the compliance piece. But reading it well and crafting a story is what becomes most important when communicating back to your board and potential donors. Here’s what you need to know and how to frame each piece:

1. Revenue concentration. If 70% or more of revenue comes from a single funder or grant, the SOA, this could be a sign of fragility. But it can also be a good way to show the board that you need more funding diversification and garner their support.

2. Expense ratios. What percentage of total expenses is program vs. overhead? Too low overhead can signal underinvestment in staff and systems. Make sure you can tell a story about where your money is going and why, each dollar accounted for.

3. Change in net assets. There is some wiggle room here in what’s acceptable. A surplus with mostly restricted funds still means thin operating flexibility. A deficit with a board-approved drawdown plan and a clear rationale could be a defensible financial position. But the number only makes sense with context.

According to the Nonprofit Finance Fund’s 2025 State of the Sector survey, 36% of nonprofits ended 2024 with an operating deficit — the highest rate in 10 years. If yours shows a deficit, you’re not alone, but you do need a plan.

4. Monthly review. Review this report monthly, not just at year-end, and always alongside your budget vs. actual. An SOA that only gets attention in February is a missed management tool 11 months out of 12.

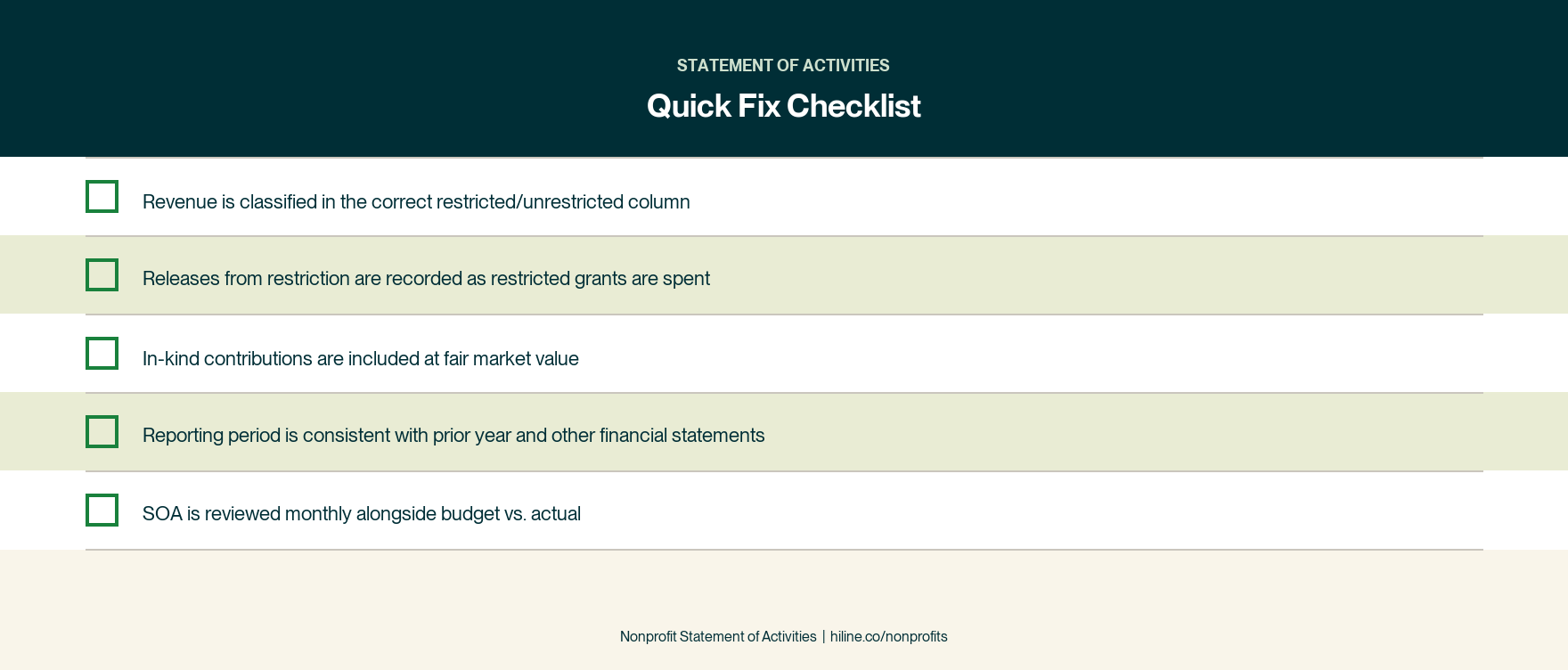

Common Statement of Activities Mistakes (And How to Fix Them)

1. Misclassifying revenue – Recording a restricted grant as unrestricted overstates available funds. Build restriction tracking into your chart of accounts from the start.

2. Forgetting releases from restriction – When restricted funds are spent as intended, the release must be recorded or restricted balances will appear artificially high.

3. Omitting in-kind contributions – Donated goods and services are real revenue and real expense. Record at fair market value even when cash never changed hands.

4. Inconsistent reporting periods – Mixing cutoffs across statements makes year-over-year comparison unreliable. Pick a period and apply it uniformly.

5. Not connecting to budget – Reviewing your SOA alongside your approved budget is the difference between a compliance document and a management tool.

If any of these mistakes sound familiar, they’re fixable. Hiline’s nonprofit accounting team helps organizations build the systems to get it right. Book a free call.

How the Statement of Activities Fits With Your Other Financial Statements

1. Statement of Financial Position (balance sheet) – A snapshot of assets and liabilities at a point in time. Ending net assets on your SOA must tie to this statement exactly.

2. Statement of Cash Flows – Your SOA can show a surplus while the bank account is nearly empty, especially when restricted grant receipts arrive ahead of the spending. The cash flow statement explains the gap.

3. Statement of Functional Expenses – Breaks expenses into program vs. overhead in greater detail, required under GAAP for most nonprofits, and feeds directly into Form 990 Part IX. Total expenses must reconcile with your SOA.

Frequently Asked Questions

What is a nonprofit statement of activities?

A nonprofit statement of activities is a financial report that summarizes an organization’s revenue, expenses, and change in net assets over a specific period, usually a fiscal year. It is the nonprofit equivalent of an income statement, required under GAAP and for IRS Form 990 filing.

Is the statement of activities the same as an income statement?

Yes, functionally the same report. “Income statement” applies to for-profit businesses; “statement of activities” is the nonprofit term. The key difference: nonprofits report changes in net assets rather than profit, and must separate restricted from unrestricted funds.

What does “change in net assets” mean on a statement of activities?

The difference between total revenue and total expenses for the period. Positive means a surplus; negative means a deficit. A surplus doesn’t mean those funds are freely available. Restricted portions must still be used as directed.

What is the difference between restricted and unrestricted funds on a statement of activities?

Funds without donor restrictions can be used for any mission-related purpose. Funds with donor restrictions must be used as the funder specified. The SOA separates these into two columns so readers can see how much of your revenue and net assets are truly flexible.

How often should we review our statement of activities?

At minimum, monthly. Monthly review lets you compare actual results against budget, spot trends early, and catch errors before year-end. Many nonprofits present a simplified version at each board meeting.

What other financial statements are required alongside the statement of activities?

Under GAAP: the statement of financial position, the statement of cash flows, and the statement of functional expenses. All four feed into your annual Form 990.

A Clean SOA Starts With Clean Books

The statement of activities is only as accurate as the bookkeeping behind it.

That sounds obvious, but it's the part most nonprofit finance teams find out the hard way. A chart of accounts that wasn't built for fund accounting from day one means every report you pull is working from a flawed foundation. Restricted and unrestricted revenue lands in the wrong buckets. Releases from restriction get missed entirely. Expense allocations don't hold up when an auditor asks to see the methodology.

By the time a major grant renewal is due or audit prep starts, untangling months of miscoded transactions is a multi-week project. Every Finance Director who's spent a Sunday afternoon reconciling a report that should have taken twenty minutes knows exactly what that costs.

Hiline builds nonprofit accounting systems that are correct from the start — chart of accounts, fund tracking, restriction management, release recording — so the statement of activities you pull at month-end is one you can actually hand to a grant officer or board member without a week of cleanup first.

That's the difference between a financial system that produces reports and one that produces answers.

Ready to stop fighting your financial systems and start focusing on your mission? Book a free consultation.

Sign up for our newsletter.

.jpeg)

.png)

.png)